Recap: An Automatter Fireside Chat with Samir Kaji

The venture banking vet and founder of Allocate on debt, the services business, being a founder, and more.

When Halle and I started inviting folks in for fireside chats, we knew right away we wanted to have Samir Kaji join us. He has spent more than 21 years in the venture industry between SVB and First Republic Bank and has built his career around helping founders and fund managers navigate the ever evolving capital markets.

Our fireside chat took place in February. With his recent announcement of Allocate, a platform that will act as the engine to enable capital allocators of all sizes to efficiently discover, assess, and access the most interesting fund managers and products, we wanted to share some highlights, gems, and insights from our conversation. Quotes by Samir are in italics.

The venture asset class has a powerful flywheel

Tech’s ubiquity and permeation of every business means winning companies can grow much bigger, much faster than they could in the past.

“There’s so many opportunities for companies to become bigger… The size and scale of outcomes is significantly bigger than it used to be.”

For much of the past 10 years, venture portfolios were built on the assumption that firms needed a $1 billion outcome to successfully return a fund and that only generation-defining companies would grow large enough to IPO at market caps above $10 billion. But in the past few years, we’ve seen time and time and time again that public market investors are ready and willing to pay up for tech businesses and to value them on their chosen terms and on the sheer level of scale that tech enables.

The growth of venture-backed winners has expanded the LP landscape dramatically.

“The number of family offices globally today is 11,000. In 2007 there was 1,000… There are now 185,000 ultra-high-net-worth individuals worth $50 million or above. Most people are putting 10 to 20 percent of their capital on average into privates, of which half is venture capital.”

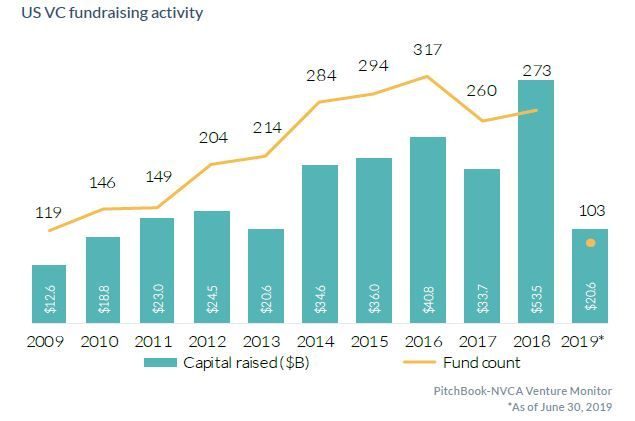

As recently as 2010, the venture asset class raised less than $20B per year. By 2016, VC broke $40B. It hit $50B just two years later. Samir believes it’s on its way to $100B per year and that larger outcomes make that level of support economically viable. Although companies are able to stay private longer than ever, earlier liquidity events -- via secondary transactions, SPACs, and acquisitions -- enable more rapid redeployment of capital back into the asset class, especially via operators who are ready to become LPs themselves.

The macro environment favors that flywheel and drives valuations higher for the most visible deals

“Right now we are looking at a big delta between what private assets can (in theory) provide and what those low-risk, low-beta securities can provide, and a lot of that is driven by interest rates… Right now, capital is cheap, and time is expensive.”

With a huge supply of capital and investors searching for growth as their north star, valuations have gone through the roof — again, supported by the prospect of larger outcomes than anyone thought possible five years ago.

But it’s worth drawing attention to the barbell effect that’s in play for companies or categories that aren’t quite as hot.

Portfolio math matters. But the growth of the biggest outcomes gives fund managers the potential to be a bit more creative with their portfolio construction.

“I’ve seen these returns for 20 years. The best [VCs] know when to flex and go outside these tight rules [on ownership targets and valuations]. Ownership matters until it doesn’t… [at the early stages] what you’re really looking at is how do I get any one company to return the fund? And then you can back into that.”

Venture banks are in the services business

“When I joined FRB in 2012, I was the first employee of this group, and our thesis was actually centered around helping emerging managers get off the ground… the number one thing that was a pain point was fundraising. How do I find all these LPs? It’s like this amorphous world of people. How do I find the right archetypes? Where are these people? It’s not like family offices hang a shingle and say I’m open for business, come find me.”

First Republic and Silicon Valley Bank help emerging managers raise money and, per Samir, they don’t charge directly for it. Like many client service businesses, they take high-touch approaches to customer acquisition and development because long-term relationships and reputations as reliable banking partners persist across time and across funds.

“In today’s world… being a licensed chartered bank is really tough, but being a front-end partnered with one of those banks is not tough… Can you create those API capabilities that integrate with things like expenses, with capital call management, with IRR calculations? That’s where banks need to go… When I left, that’s one of the things we had on our roadmap. How do we make a digital front-end that allows managers to think about things that actually go toward their fund management in terms of average check sizes, are you optimizing on your capital calls, can you sign up for a capital call line with one click of a button? All of those things are the future.”

But with tech-enabled challengers and competitors in adjacent markets, Samir sees challenges (and opportunities) for the dominant venture banks.

“These big banks are like big cruise ships or tankers. You got a lot of fintechs acting like jetskis and speedboats. They can turn really quickly. Tankers are hard to turn. They know they need to do it, but they spent hundreds of millions of dollars on systems that are hard to change. There is an opportunity for anyone who wants to create a fund bank for venture capitalists that is digital-first.”

We have to.

(Sorry.)

“If you’re banking and all you’re getting is a bank account, you need to move… I think the bar should be really high for any service provider.”

Samir described his previous role as a “copilot” for fund managers. Sometimes that meant finance-heavy work, but often it was about being the person fund managers knew they could call for questions and counsel on any topic. And that’s what he expects now as a founder himself.

Debt for startups can cost more than you think — especially if you don’t know your lender

“In the past, every company that would raise $5 or $6 million would layer on $2 million in debt. The thought would be, it extends runway… Right now, debt is cheap, and the likelihood of getting the next round of capital is probably pretty high, but environments aren’t always like that and debt can act as an anchor.”

The use of debt at startups has been a hot topic over the past year -- particularly more aggressive, more flexible, and more expensive versions of debt, such as the revenue-based financing and recurring revenue financing practiced by the likes of Pipe, Lighter Capital, and Clearbanc.

Samir called out these models and milestone-based financing as safer alternatives to the much cheaper bank debt that comes with financial covenants. If the lender doesn’t have a long track record and the agreement isn’t absolutely bulletproof in favor of the company, a founder might find themselves on the wrong side of a clause that allows the bank to pull the capital. Samir recalled a company that was doing well in 2007 but needed a bridge into 2008.

“The real estate bubble was bursting and they needed 3 more months of cash… The company walked into the bank and said, we’re about three months away from likely getting a big round, like a $20 million Series C… They had more debt than they had cash in the bank. They met with the bank, and those lenders walked out and said okay, let us think about it. Came back and said we’re just not comfortable. We’ve swept your cash.”

With the wrong lender, the wrong risk officer, and challenging circumstances, a broadly-applicable material adverse change clause can end a company. It’s hard to say if that risk is worth the limited additional runway you can get with debt.

On being a founder now

“When you come from a big company, the one thing you’re trying to avoid is you sort of operate the way you did in the big company. You’re trying to set up infrastructure and rules and protocols and it just doesn’t work. I’m just trying to get one thing right. Keep it simple.”

At Allocate, Samir doesn’t have a big team reporting to him. He is focused on doing one thing better than anyone else: Connecting LPs of all sizes with fund managers of all sizes. His challenge is to systematize and scale this model into a world where funds can be smaller, single-purpose, and syndicated; where there are 10x the number of accredited investors (and potential LPs); and where the high-touch feel of venture banking coexists with client-side automation and the convenience of consumer technology.

It’s a challenge we’re excited to see him meet and a mission we’re excited to see him fulfill.

Interested in joining a future Automatter Fireside Chat? Please take a moment to fill out our interest form!